Reinsurance could be defined as « the insurance of insurers ». In reality, it is a contract by which a specialized company (the reinsurer) assumes part of the risks underwritten by an insurer (the ceding company) from its insured. By this operation, the reinsurer commits to refund the insurer in the event of the risk materializing, a portion of the sums paid in respect of claims and receives in return a portion of the original premiums paid by the insured(s). In principle, the reinsurer only deals with insurers (B to B), which explains why Reinsurance is often unknown to the general public.

Why do insurers reinsure themselves?

As well as an insured must protect his assets (house, car….) and his family against all kinds of hazards, an insurance company must also measure and limit the exposure of its own balance sheet in order to protect its solvency margin. Every year the insurance company must estimate it’s risks, according to their frequency and probability. Once this preliminary work is done, it can better assess the needs in terms of reinsurance.

The purchase of reinsurance allows, in particular, the transfer of certain risks :

build a more homogeneous communities of risks;

protect against the volatility of the results;

limit the need for equity capital.

How is reinsurance organized?

Reinsurance is international. To play their role as regulators, reinsurers must spread their exposures globally. By reinsuring most of the world’s insurers, reinsurers are able to pool and balance their risks across the globe. There are approximately 100 reinsurers operating worldwide, with a combined turnover of approximately €338 billion in life and non-life business. Reinsurance brokers can facilitate these exchanges taking place between insurers and reinsurers. Before ceding his portfolio, the insurer must check that the reinsurer is able to settle its share of claims when they occur. To assist insurers in this task, rating agencies have specialized in controlling reinsurers solvency. Best known are S&P Global, AM Best and Moody’s. Finally, as for insurance, carrying out reinsurance activities implies obtaining an authorization based on specific approvals issued by the local supervisory authorities. In France, it is the ACPR (Autorité de Contrôle Prudentiel & de Résolution) that is responsible for this mission in the framework of the prudential rules of the European « Solvency II » regime.

How does reinsurance work?

There are two main types of reinsurance:

“Treaty » or « compulsory » reinsurance The aim is then to reinsure a community of risks (for example, an entire portfolio of motor policies) rather than a single risk.

Reinsurance treaties are negotiated in advance before their date of inception (generally 1st January) and are mandatory , meaning there is an obligation to cede all policies in the related portfolio for the insurers and an obligation to accept them for the reinsurer.

“Facultative reinsurance » In this case, the aim is to reinsure a specific risk (e.g. a factory) vs a portfolio of risks.

The particularity of « facultative » reinsurance is that the insurer can decide to cede the risk or not and the reinsurer the choice to accept it or not.

Worldwide reinsurance

2022 figures – AM Best Market Reinsurance (August 2023) & Aon reinsurance aggregate source

338 Mds€

Total premiums

Total premiums

Cumulative life and non-life premiums written by reinsurers

231 Mds€

Non-life premiums

Non-life premiums

Non-life premiums written by reinsurers

107 Mds€

Life premiums

Life premiums

Life premiums written by reinsurers

95,6%

Non-life combined ratio

Non-life combined ratio

Outflows ratio (management costs + commissions paid + losses paid + losses reserves) to inflows (earned premi)

493 Mds€

Capital

Capital

Cumulative capital of reinsurers

100

Global reinsurers

Global reinsurers

Companies specializing in reinsurance underwriting

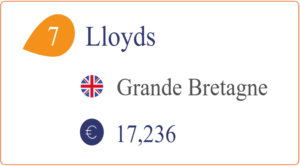

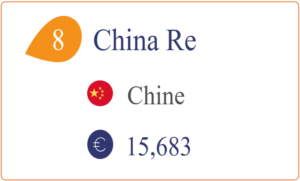

Major Global Reinsurers

Net preniums in billions of euros (2022) - AM Best Source